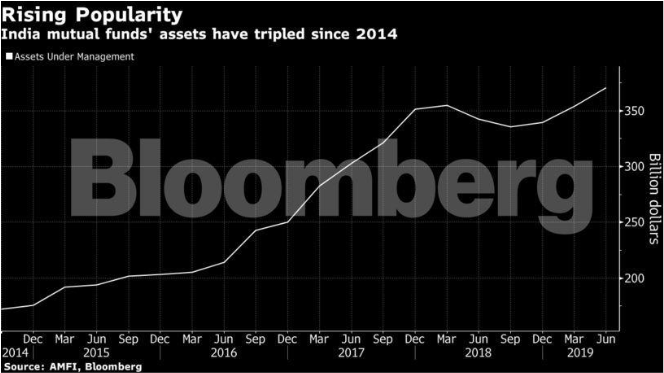

Mutual funds are one of the most popular saving avenues for investors in India. They give good returns, are inflation adjusted, provide liquidity and come in various types to suit the different risk profiles of different investors. In fact, as per the data issued by the Association of Mutual Funds in India (AMFI) and Bloomberg, since the year 2014, mutual fund accounts of individual investors have grown more than twice to 84 million. On the other hand, industry assets have tripled to USD 370 billion. Have a look –

(Source: Economic times)

These numbers strongly suggest that mutual fund investments are growing every year because of their popularity.

You would, therefore, find customers readily for selling mutual funds. However, mutual funds, like any other investment avenue, are a bit technical in nature. Your clients would be concerned with the returns of the scheme but you need to understand the working of the scheme so that you can sell the most appropriate scheme to your clients. This requires technical knowledge of mutual fund schemes. Here are, therefore, seven most important mutual fund terms which you should know before you set out to sell such schemes –

- Asset Management Company (AMC)

An Asset Management Company is the company which is responsible for handling the investment of the mutual fund portfolio to generate returns. The company is registered with SEBI and it employs fund managers to manage the investment of mutual fund schemes.

- AUM

AUM stands for Assets under Management. AUM is expressed as an absolute amount of money and represents the current market value of the mutual fund portfolio. A high AUM means that the portfolio is large showing that there are many investors in the mutual fund scheme and also that the fund has grown at a good rate.

- Entry and exit loads

Entry and exit loads are applicable when an investor invests in the scheme or redeems it. Entry load is applicable at the time of investment into the scheme. The load is charged to pay the brokerage to mutual fund distributors or brokers who have sold the scheme. The load is also charged for meeting the administrative expenses which are incurred by the mutual fund house when the scheme is sold. It is expressed as a percentage and the percentage is calculated on the amount invested. For instance, if the entry load is 1% and an investment of INR 10,000 is made, the load would be calculated as 1% of INR 10,000 which is INR 100. This load would be deducted from the invested amount to get the net investment. In the example, the net investment would be INR 9900.

Exit load, on the other hand, is the charge deducted from the fund value when the mutual fund is redeemed. This load is usually applied if you exit from the scheme within a short period. This load is also expressed as a percentage and the amount is calculated as a percentage of the redemption value. So, if you redeem your mutual fund whose value is INR 20,000 and there is an exit load of 1%, INR 200 would be deducted from the proceeds and you would get a net amount of INR 19,800.

- Open and close ended mutual fund schemes

Mutual fund schemes can be open ended or close ended. Open ended schemes are those which are open for investment for an indefinite time. There is no specific time for redeeming the funds invested in open ended mutual fund schemes. Investors can invest and redeem anytime that they want.

Close ended schemes are those where investments are done with a specified time period. These schemes, therefore, have a specified investment tenure during which redemption is not allowed. For instance, ELSS (Equity Linked Saving Scheme) schemes are a type of close-ended scheme wherein investments cannot be redeemed during the lock-in period of 3 years.

- SIP, SWP and STP

All these three terms represent a systematic way of investing or redeeming from a mutual fund. Let’s understand them independently –

- SIP means Systematic Investment Plan wherein investors can invest small, pre-defined amounts on a regular basis into the mutual fund scheme

- SWP means Systematic Withdrawal Plan wherein a specified amount is withdrawn regularly by the investor to redeem the mutual fund investment

- STP means Systematic Transfer Plan. Under this plan, initially, a lump sum investment is done in a specific mutual fund scheme. Thereafter, small, specified amounts are transferred from that mutual fund scheme to another scheme

- Expense ratio

Mutual funds pool money from investors and then invest the pooled money in different securities. The investments are also managed regularly to earn maximum returns. This management is not free of cost. Mutual funds incur fund management charges payable to fund managers and other administrative expenses in operating and managing the scheme. These charges are collected from the investors in the form of expense ratio. The total expenses incurred by the scheme are calculated as a percentage and this percentage reduces the Net Asset Value (NAV) of the fund. The NAV, therefore, is calculated after deducting the expense ratio from the market value of the portfolio and the NAV you get is the value after adjusting the expense ratio.

- NAV

NAV stands for Net Asset Value. It represents the per unit value of a mutual fund scheme. If you invest an amount in a mutual fund scheme, the NAV would determine the number of units which would be allocated to you. NAV is calculated by dividing the market value of the mutual fund portfolio by the number of securities that the portfolio holds. The formula is as follows –

NAV = (value of the assets of the portfolio – value of the liabilities of the portfolio) / number of securities held by the portfolio

NAV is dynamic and changes constantly. It helps investors assess the performance of the fund. Investment and redemption of mutual funds are done at the prevailing NAV. These terms are some of the most basic terms related to mutual fund investments. Grasp complete knowledge of these terms so that you can easily sell the best mutual funds to your clients for their needs.